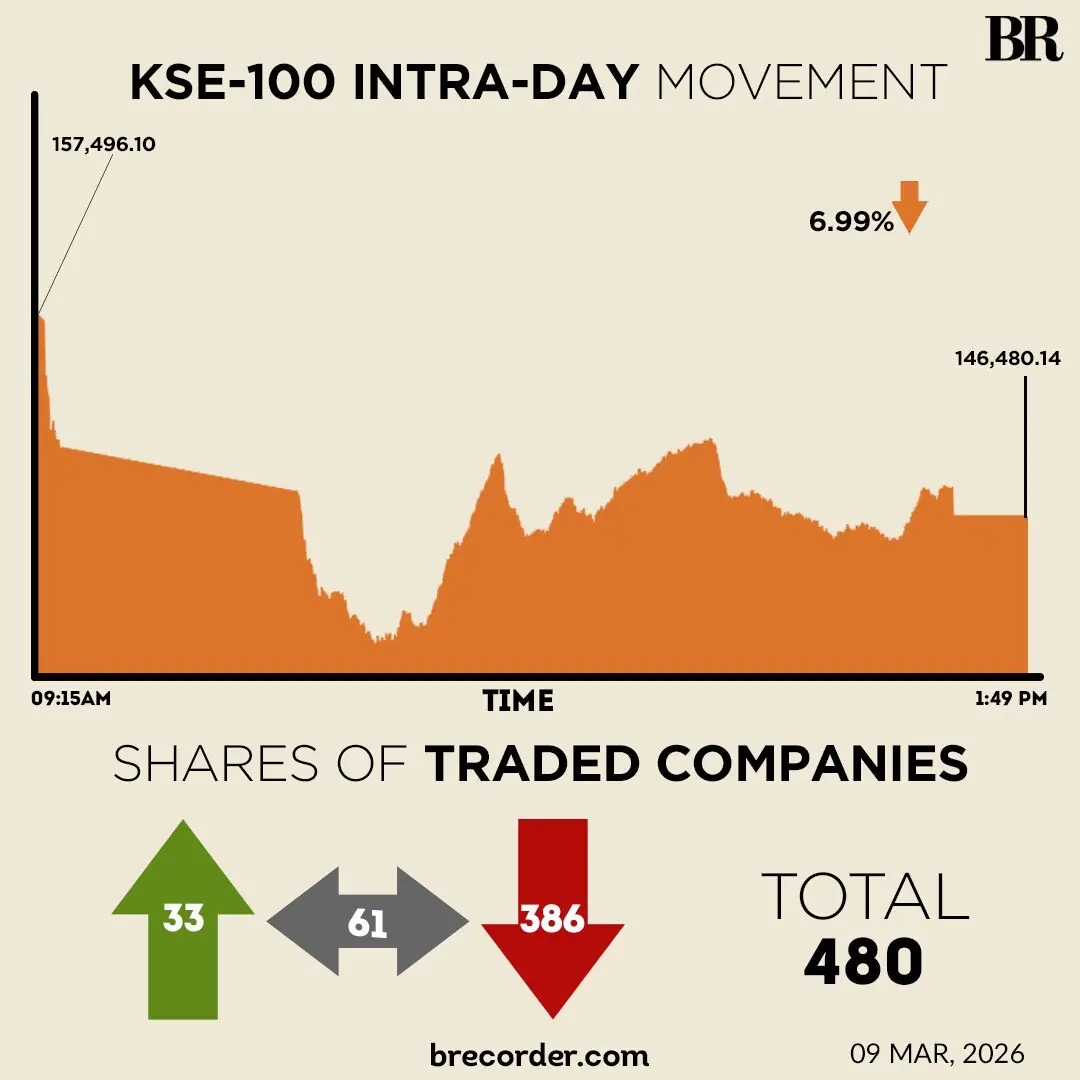

It was yet another day of intense selling pressure at the Pakistan Stock Exchange (PSX) as deteriorating geopolitical issues took a toll on investor sentiments. The benchmark KSE-100 Index registered a sharp decline of over 11,000 points during trading on Monday.

The market experienced an aggressive sell-off from the opening minutes, causing the index to drop 9,780.15 points, or 6.21% by 9:22am.

Following the decline, a Market Halt was triggered, and all equity-based markets were suspended.

“All TRE Certificate Holders are hereby informed that due to a 5% decrease in the KSE-30 index from the previous trading day close of the same, a Market Halt has been triggered as per PSX Regulations and all equity-based markets have been suspended accordingly,” read the notice.

The market resumed trading at 10:22am.

However, the index continued to slide during the early session, hitting its intraday low of 144,119.43 as selling pressure intensified.

Following the sharp fall, the market showed some recovery during midday. However, the rebound remained limited, and the index moved sideways with mild volatility during the afternoon session.

At close, the KSE-100 Index settled at 146,480.14, a decrease of 11,015.96 or 6.99%.

This was the benchmark index’s second-highest single-day decline. “Notably, the three largest single-day declines in the index’s history have all occurred in 2026,” said Topline Securities.

“This reflects heightened investor anxiety amid escalating geopolitical tensions and policy uncertainty,” Waqas Ghani of JS Global, told media.

“Markets react swiftly to risk, and the current environment has triggered a defensive shift toward liquidity and capital preservation. Restoring investor confidence will require de-escalation of regional tensions, which are sadly not in sight at the moment,” he added.

Moreover, elevated oil prices are highly detrimental to the country’s external account, and persistently high commodity prices are likely to trigger a new wave of inflation, warned Ghani.

Saad Hanif, Head of Research at Ismail Iqbal Securities Limited, also blamed the regional tensions for the market downfall.

“At this stage, the trajectory of the Iran–Israel–US situation remains uncertain, and markets typically stay sensitive to geopolitical headlines during such periods.

“The key channel through which this conflict affects the global economy is energy prices, particularly oil, given the strategic importance of the Middle East in global supply.

“Any escalation that disrupts supply or creates risks around major shipping routes could push oil prices higher, which would be inflationary for most economies and add pressure on global growth and financial markets.”

Hanif was of the view that uncertainty may persist in the near term, keeping risk premiums elevated across commodities and equities. However, if the situation remains contained without major supply disruptions, markets could gradually stabilise as investors reassess the fundamental outlook, he added.

Across-the-board selling pressure was observed in key sectors, including automobile assemblers, cement, commercial banks, oil and gas exploration companies, OMCs, power generation and refinery. Index-heavy stocks, including MCB, MEBL, NBP, MARI, OGDC, PPL, PSO, SNGPL, SSGC and HUBCO, traded in the red.

During the previous week, Pakistan’s stock market extended its sharp decline as heightened geopolitical tensions, domestic security concerns and macroeconomic uncertainty weighed heavily on investor sentiment.

The benchmark KSE-100 Index dropped 10,566.08 points, or 6.3% week-on-week, closing at 157,496.09 points compared with 168,062.17 points last week.

International, share markets nosedived in Asia on Monday as the inflationary shock from surging oil prices threatened to raise living costs and perhaps interest rates across the globe, while an investor hunger for liquidity kept the US dollar in demand.

Brent soared 23% to $114.36 a barrel, the biggest daily gain since at least 1988, which came on top of a 28% rise last week.

US crude shot up a staggering 27% to $115.11, threatening to push petrol prices quickly skyward.

Iran named Mojtaba Khamenei to succeed his father, Ali Khamenei as supreme leader, signalling that hardliners remained firmly in charge in Tehran a week into its conflict with the US and Israel.

That was unlikely to be welcomed by US President Donald Trump, who had declared the son “unacceptable.”

With no sign of an end to hostilities in the Middle East and tankers still not daring to cross the Strait of Hormuz, investors were bracing for a long stretch of higher energy costs.

All of this was sobering news for Japan, a major importer of oil and gas, knocking the Nikkei down 7.5% on top of a 5.5% drop last week.

South Korea’s high-flying market fell closer to earth with a drop of 8.1%, having already shed more than 10% last week.

China is another big oil importer, though it also has a huge stockpile of crude; its blue-chip index fell 2.3%.

China on Monday said inflation had already picked up in February ahead of the current oil spike, with consumer prices rising 1.3% on the year. This is not necessarily a negative development, given that the country has long struggled with disinflation.

Meanwhile, the Pakistani rupee registered a marginal gain, appreciating 0.01% against the US dollar in the inter-bank market on Monday. At close, the local currency settled at 279.37, a gain of Re0.03 against the greenback.

Volume on the all-share index jumped to 621.65 million from 363.14 million recorded in the previous close.

The value of shares increased to Rs37.12 billion from Rs23.11 billion in the previous session.

K-Electric Ltd. was the volume leader with 127.47 million shares, followed by F. Nat.Equities with 33.61 million shares, and B.O.Punjab with 33.39 million shares.

Shares of 480 companies were traded on Monday, of which 33 registered an increase, 386 recorded a fall, and 61 remained unchanged.

American Dollar Exchange Rate

American Dollar Exchange Rate