Gold fell on Friday as commodity index readjustments and a firm dollar kept the pressure on prices, with investors positioning ahead of crucial US non-farm payrolls data due later in the day.

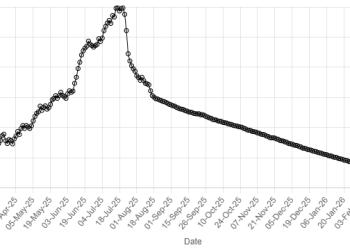

Spot gold fell 0.4% to $4,464.57 per ounce as of 0353 GMT, though it was set for a 3% weekly gain.

Bullion hit a record high of $4,549.71 on December 26.

US gold futures for February delivery firmed 0.3% to $4,473.60.

“Gold prices for the last three days, have traded off on some profit taking, but indeed a key driver at the moment is US dollar strength in advance of NFP data,” said independent analyst Ross Norman.

The US dollar advanced to a near one-month high, as traders braced for a US Supreme Court decision on President Donald Trump’s use of emergency tariff powers.

A stronger dollar makes greenback-priced bullion more expensive for other currency holders.

Economists expect modest job growth of 60,000 and a slight drop in the unemployment rate to 4.5% from 4.6%.

Prices are expected to face downward pressure over the next few days as the annual Bloomberg Commodity Index rebalancing – a periodic adjustment of commodity weightings to keep the index aligned with market conditions – begins this week.

“Several indexes are reweighting the amount of precious metals and gold in them at the beginning of the year. So to some extent there’s a bit of weakness on index rebalancing but fundamentally I think that things remain quite positive,” Norman added.

Gold prices could rise to $5,000 an ounce in the first half of 2026 on rising geopolitical risks and debt, HSBC said. Non-yielding assets tend to do well in a low-interest-rate environment and during economic uncertainties.

Spot silver lost 0.5% to $76.48 per ounce after hitting an all-time high of $83.62 on December 29.

The white metal was on track for an over 5% weekly rise.

Spot platinum shed 1.8% to $2,227.11 per ounce after scaling a record peak of $2,478.50 last Monday.

Palladium was steady at $1,786.18 per ounce. Both metals were set for weekly gains as well.

{kind=link}