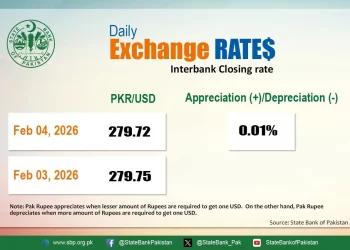

The Pakistani rupee remained largely stable against the US dollar, depreciating 0.01% during the opening hours of trading in the inter-bank market on Wednesday.

At 10:20am, the currency was hovering at 278.73, a loss of Re0.03, against the US dollar.

On Tuesday, the rupee had settled at 278.70 against the dollar, according to the State Bank of Pakistan (SBP).

In recent months, the domestic currency has largely been around 277-279 as traders keep an eye on progress with the International Monetary Fund’s (IMF) Executive Board over a new $7-billion Extended Fund Facility (EFF).

The IMF has not yet included Pakistan on the agenda of its Executive Board meetings scheduled till September 13.

According to the Fund’s website, the IMF updated the schedule of the Executive Board meeting set to be held on September 4, 6, 9 and 13, but to take Pakistan’s 37-month Extended Fund Facility (EFF) of about $7 billion on agenda is not included.

Globally, the safe-haven Japanese yen rallied on Wednesday while riskier currencies like the Australian dollar and sterling languished as traders ran for cover following the worst sell-off in almost a month on Wall Street.

The catalyst was ostensibly some soft US manufacturing data, which fanned worries about a hard landing for the world’s biggest economy, with traders already nervous ahead of crucial monthly payrolls data on Friday.

The US dollar-yen pair tends to track long-term US Treasury yields, which dropped nearly 7 basis points (bps) overnight and continued to decline in Asian hours to stand at 3.8329%, with investors flocking to the safety of bonds.

The US dollar, though, was firm against most other major peers, as it tends to draw safety flows even when the US economy is the locus of concern.

US markets had been closed for the Labor Day holiday on Monday and came back Tuesday to a weak Institute for Supply Management (ISM) survey that suggested factory activity in the country would remain subdued for a while.

Oil prices, a key indicator of currency parity, fell on Wednesday, extending a plunge of more than 4% the previous day, on expectations that a political dispute halting Libyan exports could be resolved and concerns over lower global demand growth.

Brent crude futures for November fell 37 cents, or 0.5%, to $73.38 by 0330 GMT, after the previous session’s fall of 4.9%.

US West Texas Intermediate crude futures for October were down 41 cents, or 0.6%, at $69.93, after dropping 4.4% on Tuesday.

Both contracts fell to their lowest since December on signs of a deal to resolve the political dispute between rival factions in Libya that cut output by about half and curbed exports.

This is an intra-day update

{kind=link}