The Pakistan Stock Exchange’s (PSX) benchmark KSE-100 Index closed the week’s first session positive, as the exploration and production (E&P) sector helped the index erase intra-day losses of more than 940 points on Monday.

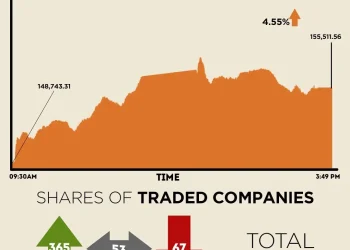

The KSE-100 witnessed selling pressure in the first half, hitting an intra-day low of 111,857.34.

However, a strong buying spree, led by the E&P sector, pushed the index to an intra-day high of 114,573.68.

At close, the benchmark index settled at 114,330.10, up by 1,529.17 points or 1.36%.

“The initial downturn was fuelled by concerns over the court’s decision to uphold the windfall tax. Market sentiment remained fragile as the Federal Board of Revenue, following the Sindh High Court’s directive, successfully recovered Rs23 billion in a single day from 16 banks, further amplifying investor unease,” brokerage house Topline Securities said in its post-market report.

“However, the tide shifted in the latter half of the session, led by a robust recovery in the E&P sector. The market staged an impressive rebound, surging to an intraday high of 1,772 points. Investor sentiment improved following reports that the government is once again prioritising the resolution of circular debt,” it added.

Media sources indicate that authorities are exploring various avenues to address the issue, including a potential Rs1.2 trillion borrowing plan from banks, capitalising on the recent decline in interest rates, according to Topline.

“Additionally, the government is keen on finalising the term sheet ahead of the International Monetary Fund (IMF) mission’s arrival, which further strengthened market confidence.”

The rally was largely driven by FFC, MCB, OGDC, PPL, and UBL, which collectively contributed 810 points to the index. Conversely, HBL, AKBL, NBP, MTL, PSX, and LCI acted as a drag, erasing 189 points from the gains, the report said.

During the previous week, PSX witnessed a positive trend on the back of local investors’ interest and institutional support. The KSE-100 increased by 715.63 points weekly and closed at 112,800.93 points.

Globally, European shares and the euro climbed on Monday as Germany’s election produced no nasty surprises, while Wall Street futures firmed on hopes results from AI diva Nvidia this week would justify the tech sector’s sky-high valuations.

DAX futures jumped 1.1%, while the single currency rose 0.5% to $1.0516 and looked set to test its January top at $0.10535. EUROSTOXX 50 futures added 0.4% and FTSE futures 0.1%.

German’s new conservative leader Friedrich Merz still has to form a coalition government and it is not yet clear whether that will include one or two partners, with the latter likely to take more time and horse-trading.

The uncertainty comes as European Union leaders are set to hold an extraordinary summit on March 6 to discuss additional support for Ukraine and how to pay for European defence needs.

Liquidity was thinned by a holiday in Tokyo markets and MSCI’s broadest index of Asia-Pacific shares outside Japan dipped 0.2%.

Nikkei futures traded at 38,310, under the cash close of 38,776.

Chinese blue chips eased 0.1%, but Hong Kong shares firmed 0.2% to extend their recent tech-driven bull run.

S&P 500 futures added 0.4% and Nasdaq futures 0.5%. The Nasdaq had fallen 2.5% last week, its worst week in three months, with losses led by the Magnificent Seven.

Meanwhile, the Pakistani rupee recorded a marginal decline against the US dollar, depreciating 0.03% in the inter-bank market on Monday. At close, the rupee settled at 279.66, a loss of Re0.09 against the greenback.

Volume on the all-share index marginally increased to 455.53 million from 455.39 million recorded in the previous close.

The value of shares rose to Rs25.89 billion from Rs21.52 billion in the previous session.

At-Tahur Ltd was the volume leader with 43.12 million shares, followed by K Electric Ltd with 27.22 million shares, and Fauji Cement with 25.76 million shares.

Shares of 440 companies were traded on Monday, of which 176 registered an increase, 211 recorded a fall, while 53 remained unchanged.

{kind=link}