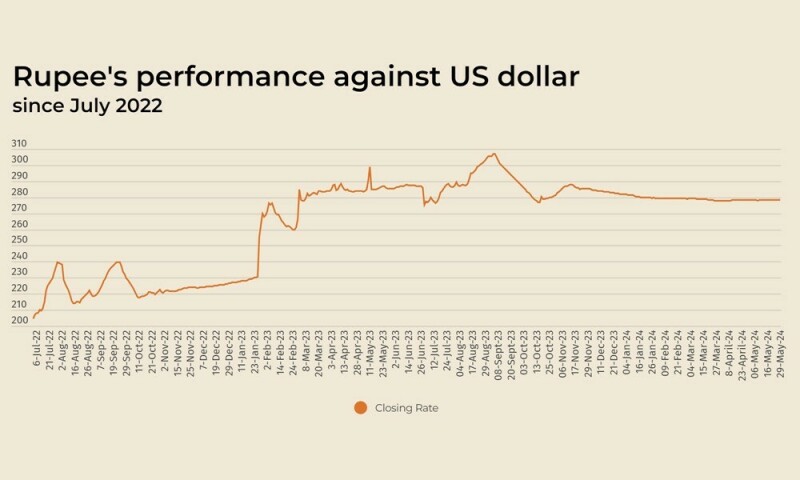

The Pakistani rupee reported a marginal decline against the US dollar, depreciating 0.04% in the inter-bank market on Wednesday.

At close, the local unit settled at 278.40, a fall of Re0.10 against the greenback, as per the State Bank of Pakistan (SBP).

On Monday, the rupee had closed at 278.30, down by Re0.09. The inter-bank market was closed on Tuesday on account of Yaum-e-Takbeer holiday.

In recent weeks, the domestic currency has largely been around 277-278 against the dollar as Pakistan moves forward with its plan to win a longer and larger International Monetary Fund (IMF) bailout programme.

Globally, the US dollar was stable on Wednesday on wagers the Federal Reserve is unlikely to cut rates until later this year ahead of crucial inflation readings this week, while the yen drifted to its weakest in four weeks.

The US dollar was also lifted by rising Treasury yields after a lacklustre debt auction for sales of two-year and five-year notes that raised doubts about demand for US government debt.

Data on Tuesday showed US consumer confidence unexpectedly improved in May after deteriorating for three straight months, but worries about inflation persisted and many households expected higher interest rates over the next year.

Against a basket of currencies, the dollar index was little changed at 104.67, inching away from the near two-week low of 104.33 it touched on Tuesday.

Oil prices, a key indicator of currency parity, rose on Wednesday on expectations that major producers will extend output cuts at a meeting on Sunday and that fuel consumption will start rising with the start of the peak summer demand season.

Brent crude futures for July delivery added 74 cents, or 0.9%, to $84.96 a barrel by 0917 GMT.

US West Texas Intermediate futures for July climbed 69 cents, or 0.9%, to $80.52. Both benchmarks gained more than 1% on Tuesday.

Traders and analysts expect the OPEC+ group comprising the Organization of the Petroleum Exporting Countries (OPEC) and allies including Russia, to keep voluntary production cuts of about 2.2 million barrels per day (bpd) in place.

The Pakistani rupee reported a marginal decline against the US dollar, depreciating 0.04% in the inter-bank market on Wednesday.

At close, the local unit settled at 278.40, a fall of Re0.10 against the greenback, as per the State Bank of Pakistan (SBP).

On Monday, the rupee had closed at 278.30, down by Re0.09. The inter-bank market was closed on Tuesday on account of Yaum-e-Takbeer holiday.

In recent weeks, the domestic currency has largely been around 277-278 against the dollar as Pakistan moves forward with its plan to win a longer and larger International Monetary Fund (IMF) bailout programme.

Globally, the US dollar was stable on Wednesday on wagers the Federal Reserve is unlikely to cut rates until later this year ahead of crucial inflation readings this week, while the yen drifted to its weakest in four weeks.

The US dollar was also lifted by rising Treasury yields after a lacklustre debt auction for sales of two-year and five-year notes that raised doubts about demand for US government debt.

Data on Tuesday showed US consumer confidence unexpectedly improved in May after deteriorating for three straight months, but worries about inflation persisted and many households expected higher interest rates over the next year.

Against a basket of currencies, the dollar index was little changed at 104.67, inching away from the near two-week low of 104.33 it touched on Tuesday.

Oil prices, a key indicator of currency parity, rose on Wednesday on expectations that major producers will extend output cuts at a meeting on Sunday and that fuel consumption will start rising with the start of the peak summer demand season.

Brent crude futures for July delivery added 74 cents, or 0.9%, to $84.96 a barrel by 0917 GMT.

US West Texas Intermediate futures for July climbed 69 cents, or 0.9%, to $80.52. Both benchmarks gained more than 1% on Tuesday.

Traders and analysts expect the OPEC+ group comprising the Organization of the Petroleum Exporting Countries (OPEC) and allies including Russia, to keep voluntary production cuts of about 2.2 million barrels per day (bpd) in place.

American Dollar Exchange Rate

American Dollar Exchange Rate{kind=link}