Dubai: UAE residents planning on taking a loan in spite of the multiple interest rate hikes – the latest being by 0.25 per cent from last Thursday – need to first make sure they get one number right.

And how they score with that number is entirely in their hands. This is about the personal credit score of the individual as measured by the Al Etihad Credit Bureau.

Prospective loan takers need to have a credit score of at least 700 points, according to senior bankers.

These days, maintaining the optimum credit score needs careful watch – with even failures to pay utility and telecom bills on time denting the score and, by extension, the individual’s chances of claiming a new loan with a local bank. The Al Etihad Credit Bureau has in the recent past made several add-ons to the scores, over and above lateness/failure to pay credit card outstanding or EMIs.

The current fixed interest rates offerings for personal loans from UAE leading banks are at 2.64 to 4.9 per cent and variable interest rates start at 3.99 and go up to 8.99 per cent.

Anything below 600 is not impressive to negotiate

– Sandeep Jadwani, Head of Investment Advisory at Habib Investment

Loan demand still high

According to the UAE Central Bank’s Q4-2022 Credit Sentiment Survey, consumer appetite for credit instruments – including for credit cards and Sharia loans – was solid. For the first three months of 2023, further increase in demand is expected across all categories of personal loans, including housing and car loans. Plus, many of the UAE’s new residents will also be tapping credit resources once they fulfill the required initial requirements.

Re-financing where possible to reduce EMI UAE banks are also topping up existing loans and offering refinancing options to clear out high-interest-bearing payments due on credit card bills and overdrafts.

These factors will keep demand for new loans high

– Prabhakar David, a former banker and CEO of Inflow Financing Broker

Keep these points in mind

A buyout is when the bank approves a personal loan to repay all previously existing loans.

Refinancing is when a borrower replaces their current debt obligation with more favourable terms.

According to David, “Loan buyouts and refinancing options are becoming increasingly popular among UAE customers. Depending on the loan applicant’s credit score, banks offer a loan top-up or extend the tenure on existing loans.” “Refinancing can be an option to reduce the EMI. In this case, the interest rate remains the same, but with a considerably lesser monthly instalment amount, those with existing loans can put that amount into savings schemes if they like.” Banks are also developing more thoughtful customer acquisition strategies. For example, some offer customers limited schemes to pay interest on their differential amounts in the case of loans on fixed deposits. For example, if you have a deposit of Dh30,000 in your bank and you need a loan of Dh100,000, you will be charged interest on the differential of Dh70,000 only.

Budgeting and savings

Personal finance experts advise UAE residents to consider taking a look at making room for savings. Planning a budget, ensuring outstanding credit debt, and creating a savings plan remain vital in ensuring individuals do not enter into a debt spiral.

Joseph El Am, General Manager, StashAway, says, “This is the first time since the 1980s that both inflation and interest rates are high. Regardless of whatever is happening in the market, it is important to adopt a realistic approach to budgeting and debt management, such as the 50-30-20 rule of savings.”

El Am suggests recurring savings and fixed deposits will help as the interest rates savers can earn on that is high.

Take this opportunity to invest in savings schemes, regardless of how the market behaves

– Joseph El Am, General Manager, StashAway

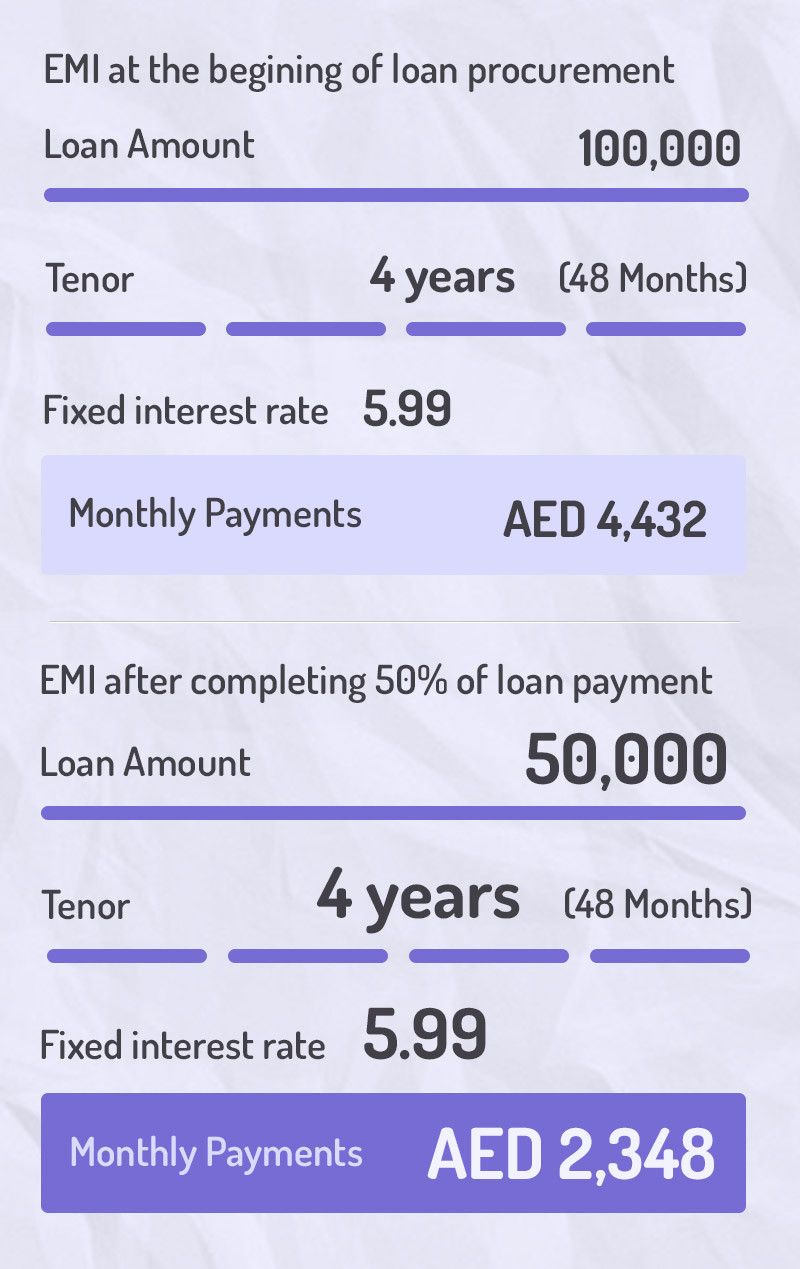

Typically, if you have taken a loan of Dh100,000 on a four-year tenor at a fixed interest rate of 5.99 per cent per annum, the monthly EMI works out to Dh4,432 per month. After two years, you would have paid off Dh50,000. With a refinancing option, the EMI can be reduced to Dh2,216 by extending the tenor to another four years.

The interest amount remains the same. Such a move also reduces the mandatory Debt Burden Ratio (DBR) for those sitting on a maximum threshold of 50 per cent. A DBR threshold is when an individual’s total debt cannot exceed 50 per cent of their monthly income. “It gives people more wiggle room to do more with their money,” says Prabhakar David Inflow Financing Broker..

{kind=link}